You

want to be future-ready and demonstrate your financial skills to the bank.

Therefore, you planned on being extra prudent regarding your credit behaviour

for a few months. You didn't borrow too much and are only taking as much credit

as you can afford to pay back. You are paying the minimum amount for all your

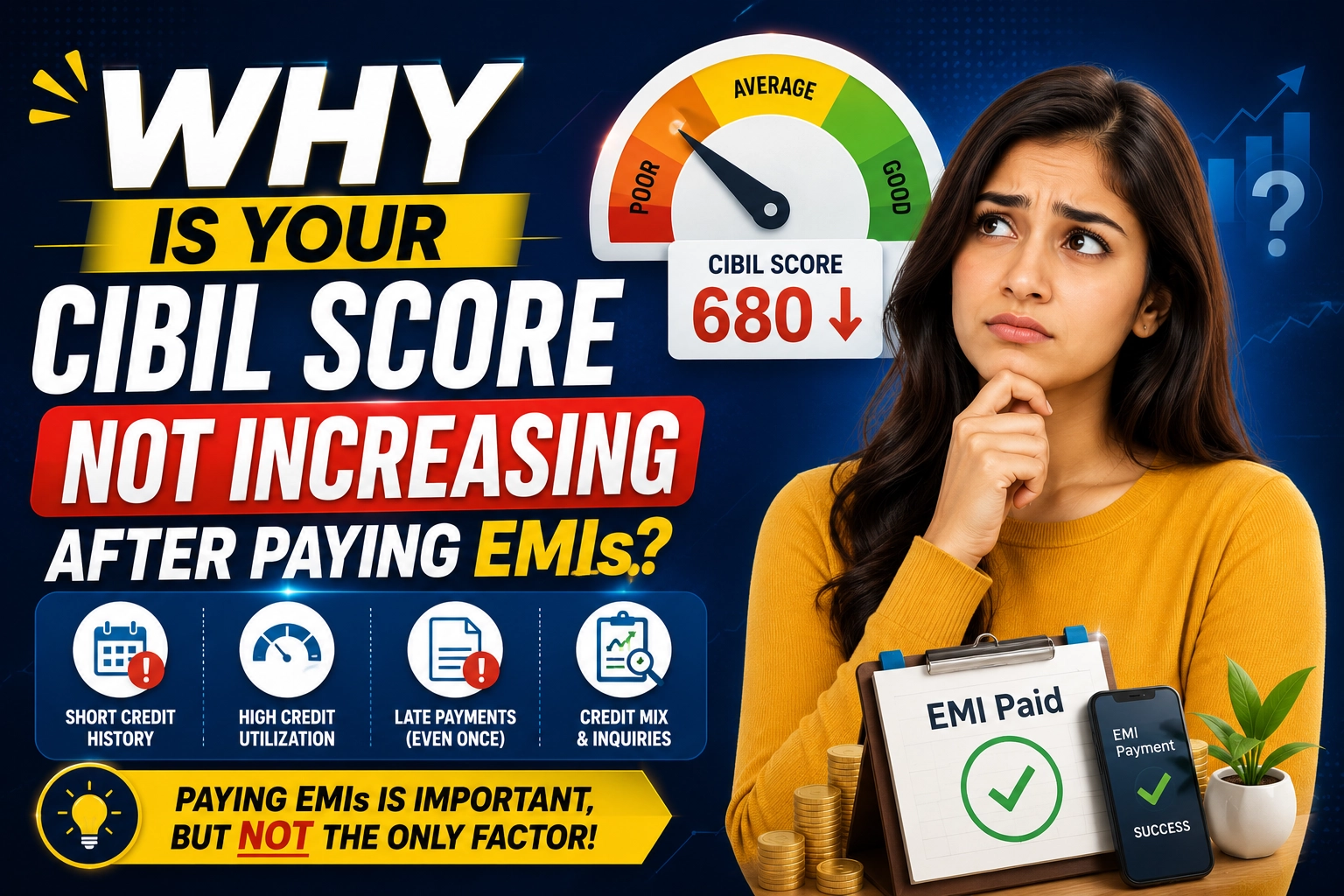

EMIs on time– the golden rule of the credit world. However, even after paying

your EMIs way before the due date, your 600 CIBIL score is not increasing.

There is no other noticeable debt or repayment behind this. What do you do? How

to increase CIBIL score from 600 to 750?

Read the ultimate guide to understand why your CIBIL score is not increasing and how to increase CIBIL score fast.

Reasons Why Your CIBIL Score Is Not Increasing

A CIBIL report is not just a number based on your repayment bills; it is a comprehensive monitoring tool that encompasses many complex aspects. A well-versed individual will understand this concept and plan their credit from all possible angles. Your payment history is just 35% of your CIBIL report. There must be something else holding you back on your credit journey. A well-rounded approach towards credit building is a must.

1. Past Debts and Defaults

Even after you removed the outstanding dues from your past negative activity, these marks can affect your overall credit score. Why? This is called the 7-year rule of CIBIL. Most of your defaults, missed payments, and settlements stay in your credit report for 7 years. This applies for the period even after you resolve these problems. This is a period given to you by CIBIL to rectify your behaviour.

This negative mark can quietly impact your overall CIBIL score. For this reason, you need even more patience to see any difference at all.

2. Only One Kind of Credit

You prefer only one type of credit and find taking on different types of credit hard to manage. What if you can’t make all the payments at the same time? You are using just one credit card to stay financially responsible. Fair enough, right?

What your credit bureau thinks is completely different. How TransUnion CIBIL perceives this behaviour is that you can’t manage all kinds of credit. Taking up an FD-backed personal loan or mortgage loan with your credit card can tell your bank and bureau that you can manage all kinds of borrowings at the same time. This practice is called the credit mix.

3. High Credit Utilisation

You are vigilant and extra careful about your instalment due dates. But you didn’t calculate your monthly credit usage. This might be the hidden factor why your CIBIL score is not increasing. Your CUR is calculated as 30% of your entire credit report. This is because your bureaus take this as overdependence on credit or trouble managing debt.

This is possible even if you take a single credit as the optimum limit. This is 30% of your entire credit limit, and ideally you should take less than this. If this payment is 25% of your limit, but your outstanding balance is ten per cent, this makes your total usage 35%, which is beyond the threshold. This is the maths that you should be aware of.

4. Errors or Incorrect/ Duplicate entries

Your CIBIL report is very likely to have errors or display wrong personal information. This could even be duplicate entries like the same loan account displayed twice, incorrect outstanding balance, or a closed account shown as written off. If you don’t check your CIBIL report regularly, you might miss these details; this can be a reason why your CIBIL score is not increasing. This applies to even personal details like name or contact information.

5. Multiple recent credit or loan applications

Every application that you make for a new loan or credit automatically counts as a hard inquiry. This means that a lender has launched a check on your credit report and history. This is to determine your past activity and creditworthiness. This is the checking process before you get approved for credit or a loan. Each hard inquiry drops your credit score, and multiple hard inquiries made together can be drastic. This also means to the banks that you are under financial stress. Even if this aspect is only 10% of your credit report, it is immediately impactful on your report.

6. Short Credit History

If you have a new credit account and haven’t made or used many credit requests yet, it might be a reason why your score is affected. Bureaus, banks and lenders need a steady, active history to determine your creditworthiness and repayment behaviours. This is how they reach a conclusion and decide whether you will be able to repay the loan or not.

7. Inactive Accounts

If your credit account is dormant and you are not using any credit card or loan, it is registered as inactive. Only your recent behaviour is used for score increases. If you have no new positive data to monitor, this will not impact your scores, even if you continue paying other EMIs. This also shortens your average account age, which is an important factor in the scoring model.

8. Old Settlements

Your settlements can still stall growth if you negotiated the final amount for repayment. This is because your account is marked as ‘settled’, not 'closed’. You first need to request the lender for full repayment and then work on improvement for a couple of months.

9. Multiple Outstanding Debts

If you are paying your current EMIs, but you have past loans piling up and increasing your total outstanding balance, it shows your CIBIL score is not increasing. This is because your due debt is still counted as pending. Even if you think that paying before time each month is enough, it could be a red flag. If you just pay the minimum every month but your overall debt balance keeps building up, it will negatively impact your score. So you should pay the full amount. If not, try to contribute as much as you can.

10. Closed Accounts

If you recently closed one of your old accounts for ease of management, you just made a huge mistake. Not only will this change remove valuable positive history of activity for bureaus, but it will also affect your ongoing and current activities. It will reduce your overall credit limit, as the limit in your old account was added to the credit limit of the new account.

How To Rectify This Hidden Growth Stall

A credit growth stall is not a dead end you can’t survive. As mentioned earlier, your credit score is a comprehensive number evaluated on multiple factors. There might be multiple reasons why your CIBIL score is not increasing. This is how to repair your credit score.

1. Strengthen your credit mix

If you clearly use only one method for credit purposes, try to make a natural credit mix of secured and unsecured loans. Add a gold loan, Fixed deposit loan or secured credit card to your profile. You shouldn't simply use multiple unsecured loans. Remember to keep a 4-6 months gap between any new applications.

2. Reduce your credit usage

Closely inspect your recent activities to find any setbacks hiding in your credit usage. CUR should be maintained between 10% and 30%.

3. File a Dispute

If you notice an error in your report that is obviously hurting your score, file a dispute. Verify your data with proof for instant score upliftment.

4. Stay More Active

Take more credits, use different types of credit, repay all your dues, and stay active for 12 months. This is a great way to strengthen your score in multiple aspects. This will improve your credit history, credit mix and overall credit score.

5. Address your outstanding dues

Instead of making small repayments, consider paying up the full amount upfront. Cleaning your slate will make you safe for new credit activity. Create a strategy instead of paying minimum amounts every month.

6. Close your settled accounts

If you simply negotiated a loan amount and considered yourself free, you are wrong. Review the ‘settled’ status in your report and request a ‘closed’ status. After this change is updated, you will see a positive impact on your low CIBIL score.

7. Use Old Accounts

Diversify your credit with new and old accounts. Don’t just use your new account for loans and credits, but use your old accounts interchangeably.

Why Is My Credit Score Not Increasing At 750?

A CIBIL score of 750 is an excellent milestone, so congratulations! The higher your credit score is, the more difficult it is to push it further. This is because you are reaching out for more responsibilities for a perfect 800 CIBIL score. This poses a fresh new challenge to you. When you are already doing everything right, what is there that is left to do?

You can analyse your report and history to see what kind of behaviour you can add for the scoring model to review. This might mean that something is keeping your stable credit score from improving. If you already have a good credit score, use the best way to maintain credit score.

Add a new credit

A new credit can contribute to your diversification. The more diverse your history is, the more skilled you are at managing new and different types of credit. This can push your score into the top range, as you are adding more skill, responsible behaviour, and value.

Increase Your Total Credit Limit

Increasing your limit will give you more area for improvement in your future borrowings. Not only will you be eligible for more credit activity, but also have reduced credit usage on average credit. The additional limit will reduce your overall usage and improve your credit score.

Avoid new hard inquiries

Stop all applications if you have garnered multiple hard inquiries. This may have frozen your score.

Reduce predictability

A credit score plateau can be fueled by inactivity or no new behaviour. Therefore, add something new to your financial habits for the bureaus to see your progress.

Remove Existing Negative Marks

As old marks can still work in the background by stopping your growth, you can rectify your old mistakes. Verify your statement with the ‘closed’ status, showing a sudden usage decrease, and make regular payments to new accounts. This will bring a slower but ensured lift in a year or two.

Credit Score Myths

Credit Score management requires patience and practical prudence to get hold of. It is easy to believe in credit score myths and stay disoriented from the correct path for credit score improvement. Below are some common credit myths, debunked.

1. Checking your credit score lowers it

A regular credit score check is one of the healthiest financial habits you can have, and it is a soft pull. It differs from a hard inquiry when a lender pulls a check on your credit report and history. Only a hard inquiry will lower your score, not a soft pull.

2. A credit card balance supports my credit score improvement

There is a thin line between credit activity and management, and actually building up balances. Credit activity to improve credit score means being careful and repaying responsibly. Having balances doesn't directly mean that you are actively repaying them. It can actually portray you as a high-risk borrower. Therefore, it is a good practice to have some gap between borrowings.

3. I don’t need my credit score until I want a loan

You need credit for emergencies, and it is also a good practice to demonstrate your financial prudence. The longer your credit history is, the better your chances at securing a loan. Even a 0.5% difference in interest rates matters, so start early.

4. To improve your credit score, close your old account

Old accounts and cards add valuable information and history to your existing credit report, so you should save them for monitoring.

5. All you need to do is pay minimum amounts on every due date

Some people think that the sole requirement is to never miss a payment. But even though you are paying every month, you are only paying the minimum threshold, while your debt balance is still increasing. You haven't really successfully made any responsible repayments yet. This is a major mistake why your CIBIL score is not increasing.

Also, remember that having a good credit score doesn’t mean your loan will be approved.

Conclusion

On the surface, it might seem to many borrowers that paying bills on time can avoid any credit score drops. But the actual practice is a much broader concept. You don't just need to be well-informed on what goes on in your credit report, but also be aware of your financial actions.

Many errors and other myths go unnoticed; therefore, regular credit report checks can be a lifesaver. Some common reasons why your CIBIL score is not increasing are outstanding dues, less diversity of credit, credit report errors and high credit utilisation.

FAQs

1. Why has my score dropped after closing an account?

After you closed your debt account, it may have reduced either your history or credit mix. Any active accounts show that you are skilled at managing debt.

2. How much time does it take for my score to increase after a settlement?

After a settlement is ‘closed’, it may take up to 12 months to see any positive change in your credit score. The time period depends on the severity of the delinquency.

3. Why do I need a credit score if I don’t need a loan?

You might not need a loan now– but you will need one in the future. You can use one not just to borrow money, but to make important decisions in your life or effectively manage your finances.

4. How to get a perfect 800 credit score?

For a perfect credit score of 800, diversify your credit, save your old account history, increase your credit limit, reduce your CUR, and limit new hard inquiries.

5. How can I create a credit mix?

You can create a credit mix by using both credit cards and loan accounts, making small, manageable purchases, and achieving credit diversity naturally.